Understanding High-Yield Savings Account Fundamentals

High-yield savings accounts represent one of the most reliable best high-yield savings accounts available to American investors seeking both security and competitive returns. These specialized deposit accounts typically offer interest rates significantly higher than traditional savings accounts, often providing returns that outpace inflation and preserve purchasing power. The fundamental appeal lies in their combination of FDIC insurance protection, liquidity, and yield that traditional checking accounts cannot match. Unlike riskier investment vehicles, these accounts provide guaranteed returns without exposure to market volatility, making them ideal for emergency funds, short-term savings goals, and cash allocations within broader investment portfolios.

The mechanics behind high-yield savings accounts involve banks utilizing online platforms to reduce operational costs, allowing them to offer more attractive interest rates to customers. Without the overhead expenses associated with maintaining physical branch networks, online banks can pass along savings through higher yields. This business model has revolutionized personal banking, creating opportunities for consumers to earn substantially better returns on their liquid assets. The accounts typically feature no minimum balance requirements after opening, though some institutions may require initial deposits ranging from $1 to $500 to establish the relationship. Understanding these operational advantages helps investors appreciate why online banks consistently outperform traditional brick-and-mortar institutions in yield offerings.

Federal Deposit Insurance Corporation coverage provides crucial security for high-yield savings account holders, protecting deposits up to $250,000 per account ownership category. This government backing ensures that even in the unlikely event of bank failure, investors’ principal remains secure. The insurance coverage applies equally to online and traditional banks, provided they maintain FDIC membership. This safety net allows investors to pursue higher yields without sacrificing the security that characterizes more conservative banking products. The combination of competitive yields, full insurance protection, and immediate access to funds creates an attractive proposition for investors across all wealth levels and financial objectives.

Top-Performing Savings Account Options for 2025

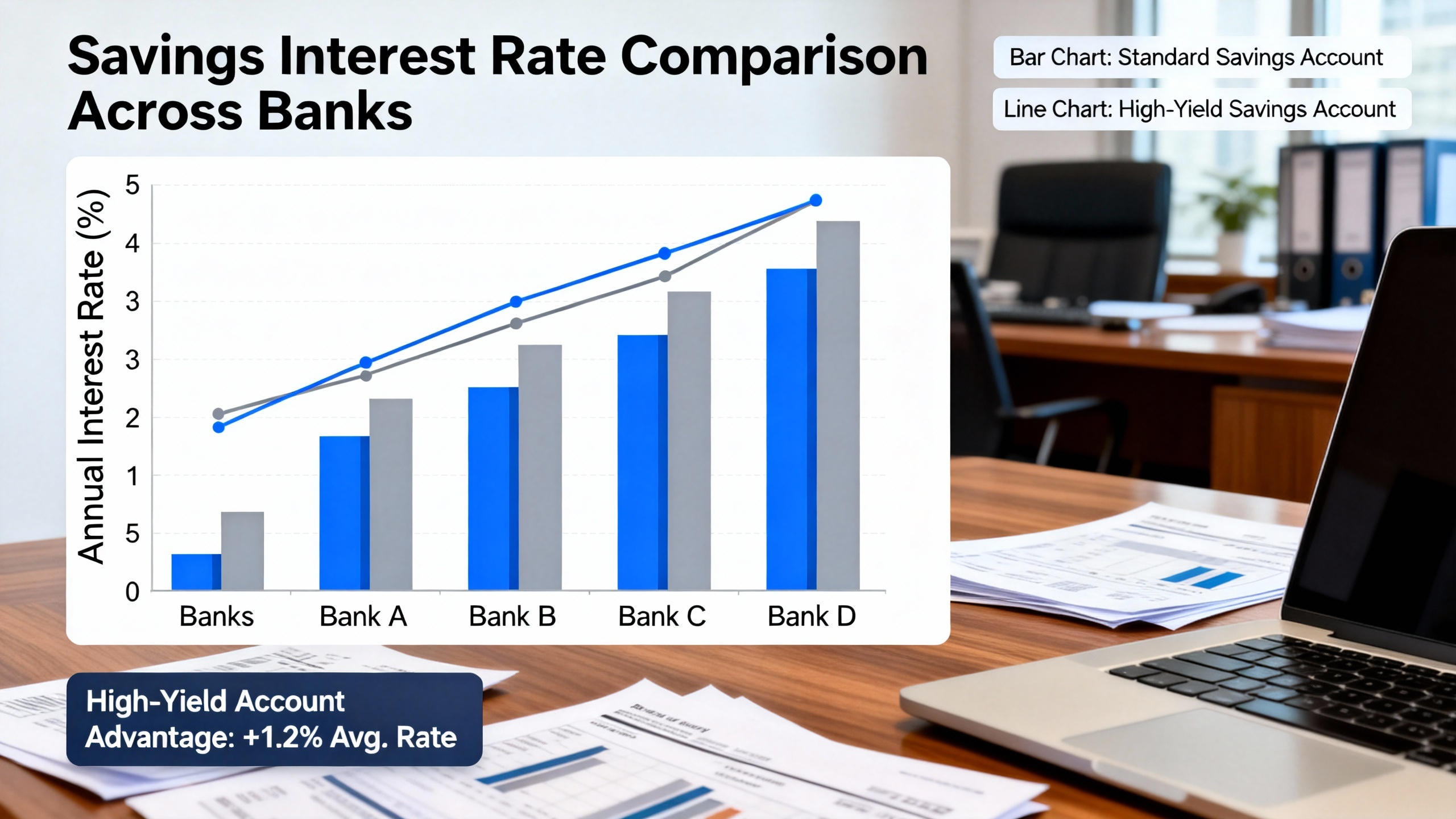

The competitive landscape for high-return savings vehicles continues to evolve, with several institutions distinguishing themselves through exceptional yield offerings, user experience, and additional benefits. Online banks consistently lead the market, with many offering annual percentage yields between 4.00% and 5.25% on savings balances. These rates substantially exceed the national average for traditional savings accounts, which typically languish below 0.50% APY. The disparity highlights the importance of actively seeking out competitive options rather than settling for convenience with familiar brick-and-mortar institutions. Savvy investors recognize that moving funds to higher-yielding accounts can generate meaningful additional income without accepting additional risk.

Several categories of financial institutions excel in the high-yield savings space, each with distinct advantages for different types of investors. Pure online banks often offer the highest outright yields, leveraging their low-cost structures to maximize returns for customers. Credit unions provide competitive alternatives, with some offering exceptional rates on smaller balances through special promotions or relationship-based pricing. Fintech companies partnering with FDIC-insured banks combine technological innovation with banking security, creating seamless user experiences alongside attractive yields. Traditional banks with robust online divisions offer middle-ground solutions, blending physical presence accessibility with competitive digital offerings. Understanding these institutional differences helps investors select options that align with their preferences for yield, service, and accessibility.

The evaluation process for top savings accounts extends beyond headline interest rates to include several critical factors that impact overall experience and returns. Account fees represent a primary consideration, with the best options eliminating monthly maintenance fees, minimum balance penalties, and excessive transaction charges. Transfer capabilities and processing times affect liquidity management, with faster transfer options providing greater flexibility. Mobile application functionality and online banking features influence usability, particularly for investors accustomed to managing finances digitally. Customer service accessibility and quality contribute to problem resolution efficiency, while additional features like sub-account creation for goal tracking enhance organizational capabilities. These comprehensive evaluations ensure selected accounts deliver both competitive yields and superior overall banking experiences.

Strategic Allocation Within Savings Portfolios

Effective utilization of best high-yield savings accounts requires strategic thinking about fund allocation within broader financial plans. These accounts serve multiple purposes within comprehensive wealth management strategies, each demanding different allocation approaches. Emergency funds typically represent the foundation, with most financial advisors recommending three to six months’ worth of living expenses maintained in highly accessible, secure accounts. The high-yield nature of these accounts ensures emergency reserves maintain purchasing power while remaining immediately available when needed. This approach contrasts with traditional savings methods that often saw emergency funds languish in low-yield accounts, effectively losing value to inflation over time.

Short-term savings goals benefit significantly from high-yield account allocation, providing dedicated vehicles for objectives with one to five-year time horizons. Common applications include down payment savings, vehicle purchase funds, vacation budgeting, and home improvement reserves. The separation of these funds into dedicated accounts creates psychological barriers against impulsive spending while ensuring dedicated progress tracking toward each goal. Many high-yield savings platforms offer sub-account features that facilitate this organized approach within single banking relationships. The competitive yields accelerate goal achievement compared to traditional savings methods, potentially shaving months or years off target dates through compounded interest accumulation. This systematic approach transforms abstract financial goals into tangible, achievable targets with clear funding roadmaps.

Cash management within investment portfolios represents another strategic application for high-yield savings accounts. Investors often maintain cash positions for opportunity capture, risk management, or tactical allocation purposes. Parking these funds in high-yield accounts ensures they contribute to overall portfolio returns rather than acting as drags on performance. The liquidity features allow quick deployment when investment opportunities arise, while the security aspects preserve capital during market downturns. This approach proves particularly valuable during periods of market uncertainty or elevated valuations, when maintaining elevated cash positions becomes prudent. The integration of high-yield savings into broader investment strategies demonstrates sophisticated cash management that maximizes returns across all portfolio components, not just risk assets.

Digital Banking Platforms and Technological Integration

The evolution of no-fee investment platforms has dramatically transformed the high-yield savings landscape, creating seamless digital experiences that prioritize user convenience and efficiency. Modern online banking platforms offer comprehensive feature sets that rival or exceed traditional banking services, including mobile check deposit, instant balance updates, and real-time transaction monitoring. The elimination of physical branch requirements has enabled institutions to invest heavily in digital infrastructure, resulting in sophisticated applications that handle everything from account opening to complex money movement with minimal friction. This technological advancement has democratized access to high-quality banking services, regardless of geographic location or previous banking relationships.

Security features within digital banking platforms have advanced significantly, incorporating multi-factor authentication, biometric verification, and real-time fraud monitoring to protect account holders. These measures often exceed the security protocols available at physical branches, where traditional identification methods remain more vulnerable to exploitation. The encryption standards employed by reputable online banks ensure that sensitive financial information remains protected during transmission and storage. Account holders benefit from immediate notifications of suspicious activity, allowing rapid response to potential security threats. The combination of advanced technology and vigilant monitoring creates banking environments that are both highly convenient and exceptionally secure, addressing common concerns about digital banking safety.

Integration capabilities represent another significant advantage of modern digital banking platforms, with many offering application programming interfaces that connect with personal finance optimization apps and accounting software. These connections allow automated tracking of savings progress, categorization of transactions, and synchronization with broader financial management systems. The automation reduces manual data entry requirements and minimizes errors in financial record-keeping. Many platforms also offer application programming interfaces that enable developers to create custom integrations for specific financial management needs. This interoperability transforms high-yield savings accounts from isolated banking products into integrated components of comprehensive financial ecosystems, enhancing their utility within sophisticated wealth management strategies.

Automated Savings Strategies and Behavioral Finance

The implementation of money management automation represents a revolutionary approach to consistent wealth accumulation through high-yield savings accounts. Automated transfer systems allow investors to establish recurring deposits that align with pay schedules, financial goals, and cash flow patterns. This systematic approach eliminates the willpower requirement from saving decisions, transforming wealth building from sporadic manual transfers into consistent automated processes. The psychological benefits of automation cannot be overstated, as they overcome common behavioral finance pitfalls like procrastination, forgetfulness, and emotional spending decisions. By making savings automatic, investors ensure consistent progress toward financial objectives regardless of daily money management moods or distractions.

Behavioral finance principles inform several innovative features within modern high-yield savings platforms that enhance saving effectiveness. Round-up programs automatically transfer small amounts from checking account transactions to savings, capitalizing on the psychological principle that small, frequent transfers feel less impactful than large lump sums. Goal-setting features with visual progress trackers leverage the endowment effect and goal-gradient hypothesis, increasing motivation as targets approach. Notification systems that celebrate savings milestones provide positive reinforcement that encourages continued disciplined behavior. These features transform the often abstract concept of saving into tangible, engaging experiences that align with how people actually think about and interact with money in daily life.

The integration of artificial intelligence and machine learning into savings platforms has created personalized recommendation engines that optimize saving strategies based on individual financial behaviors and patterns. These systems analyze income, spending, and saving data to suggest ideal transfer amounts, timing, and allocation across different goals. They can identify opportunities to increase savings during periods of lower spending or higher income, creating dynamic saving plans that adapt to changing financial circumstances. Some platforms offer predictive features that forecast future account balances based on current saving rates and spending patterns, providing valuable insights for financial planning. This technological sophistication transforms high-yield savings from passive banking products into active financial partners that actively work to maximize account holder wealth accumulation.

Interest Rate Environment Considerations

The performance of high-return savings vehicles remains intimately connected to broader interest rate environments determined by Federal Reserve monetary policy. Understanding this relationship helps investors set realistic expectations and make informed decisions about account selection and fund allocation. During periods of rising interest rates, high-yield savings accounts typically offer increasingly attractive yields as banks adjust rates to remain competitive and manage their deposit bases. Conversely, during declining rate environments, yields may decrease, though they generally remain superior to traditional banking products. This dynamic nature distinguishes savings accounts from fixed-rate products like certificates of deposit, offering flexibility alongside yield potential.

The current interest rate landscape favors savers, with Federal Reserve policies maintaining elevated rates to combat inflationary pressures. This environment creates exceptional opportunities for investors to earn meaningful returns on liquid assets without accepting market risk. The spread between high-yield savings rates and inflation rates determines the real return on savings, with positive real returns indicating preserved purchasing power. Monitoring economic indicators like consumer price index reports, Federal Open Market Committee statements, and employment data provides insights into potential future rate movements. This macroeconomic awareness helps investors make strategic decisions about locking in longer-term rates through certificates of deposit or maintaining flexibility with savings accounts during uncertain rate environments.

Comparative analysis between savings account yields and alternative short-term investment options ensures optimal capital allocation decisions. Money market funds often provide comparable yields to high-yield savings accounts but may lack FDIC insurance protection. Treasury bills offer government backing and competitive rates but involve more complex purchasing processes and potential liquidity considerations. Certificate of deposit ladders provide higher guaranteed rates for specific terms but sacrifice flexibility compared to savings accounts. Understanding these trade-offs allows investors to construct blended cash management strategies that optimize returns, liquidity, and security based on individual circumstances and market conditions. This comprehensive approach ensures that every dollar works as efficiently as possible within overall financial plans.

Tax Efficiency and Reporting Considerations

The interest income generated from best high-yield savings accounts carries specific tax implications that investors must understand for proper financial planning and compliance. Unlike tax-advantaged retirement accounts, savings account interest receives ordinary income tax treatment at both federal and state levels. This means interest earnings get added to other income sources and taxed at marginal tax rates, which can range from 10% to 37% depending on overall income levels. The tax treatment makes yield optimization particularly important for investors in higher tax brackets, where the after-tax return ultimately determines the actual benefit received from savings account allocations.

Financial institutions provide annual tax documentation through Form 1099-INT, which reports the total interest earned during the calendar year. This form must be included when filing income tax returns, with the interest amount added to other income sources. Proper record-keeping ensures accurate reporting and simplifies tax preparation processes. Investors maintaining multiple savings accounts should consolidate 1099-INT forms from all institutions to ensure complete income reporting. The simplicity of savings account tax reporting contrasts with more complex investment income reporting, making these accounts attractive for investors seeking straightforward income generation without complicated tax consequences. This transparency allows for easy projection of after-tax returns when comparing different savings options.

Strategic placement of savings within different account types can optimize overall tax efficiency for investors with multiple banking relationships. Those in higher tax brackets might prioritize municipal money market funds or other tax-exempt options for portions of their cash allocations, though these alternatives may sacrifice FDIC insurance protection. The trade-off between tax efficiency and security requires careful consideration based on individual risk tolerance and tax situations. For most investors, the combination of FDIC insurance and competitive pre-tax yields makes high-yield savings accounts the optimal choice for emergency funds and short-term savings, despite the tax implications. This balanced approach ensures security and accessibility while maximizing returns within appropriate risk parameters.

Emergency Fund Optimization Strategies

The construction and maintenance of emergency funds represent one of the most critical applications for high-return savings vehicles, combining security, accessibility, and yield in optimal proportions. Traditional emergency fund guidance suggested keeping three to six months’ worth of living expenses in liquid accounts, but high-yield options allow these reserves to generate meaningful returns rather than languishing in non-productive accounts. The determination of appropriate emergency fund size should consider individual circumstances including job stability, income variability, insurance coverage, and potential unexpected expenses. Those with irregular income or higher financial obligations might maintain larger buffers, while those with stable employment and comprehensive insurance might opt for smaller reserves.

The tiered emergency fund approach represents a sophisticated strategy that optimizes both returns and accessibility. The first tier maintains immediate cash needs in checking accounts or physical savings for instant access. The second tier allocates one to two months’ expenses in high-yield savings accounts accessible within one business day. The third tier places additional reserves in slightly less liquid but higher-yielding instruments like short-term certificates of deposit or Treasury bills. This layered structure ensures immediate needs are covered while maximizing returns on portions of the emergency fund that statistically are less likely to be needed immediately. The psychological comfort of knowing funds are both productive and accessible reduces financial stress and encourages consistent saving behavior.

Regular reviews and adjustments of emergency fund allocations ensure they remain appropriate as life circumstances evolve. Major life changes like marriage, home ownership, children, or career transitions typically warrant emergency fund reassessment and potential increases. Economic environment changes might also influence ideal emergency fund size, with periods of economic uncertainty suggesting larger buffers. The high-yield nature of modern savings accounts reduces the opportunity cost of maintaining larger emergency reserves, making over-saving less financially punitive than in previous low-rate environments. This flexibility allows investors to err on the side of caution without significantly impacting overall portfolio performance, providing peace of mind alongside competitive returns.

Relationship Banking and Additional Benefits

Many financial institutions offering best high-yield savings accounts extend relationship benefits that enhance overall banking experiences beyond competitive interest rates. These perks often include waived fees on other banking products, preferred rates on loans, and enhanced customer service access. The consolidation of banking relationships can simplify financial management while unlocking additional value through bundled services. Understanding these relationship benefits helps investors select institutions that align with broader financial needs rather than focusing exclusively on savings account yields. This holistic approach often delivers greater overall value than chasing marginal yield differences between similar accounts at different institutions.

Common relationship benefits include premium checking accounts with waived monthly fees, reimbursement of out-of-network ATM charges, and free cashier’s checks or money orders. Some institutions offer credit card bonuses with enhanced rewards rates or sign-up bonuses for maintaining certain deposit levels. Mortgage and loan rate discounts represent valuable benefits for investors anticipating future borrowing needs. The integration of these services creates comprehensive financial ecosystems that handle everything from daily banking to major financial transactions within single relationships. The convenience of consolidated banking often outweighs small yield differences, particularly when considering the time savings and simplified financial management that result from relationship consolidation.

The evaluation of relationship benefits should consider both quantitative and qualitative factors beyond straightforward monetary value. The quality of mobile banking applications, customer service responsiveness, and problem resolution efficiency contribute significantly to overall banking satisfaction. The stability and reputation of the financial institution provide assurance about long-term relationship viability. Additional features like estate planning services, financial advisory access, or business banking integration might provide value for investors with complex financial situations. This comprehensive evaluation ensures selected banking relationships deliver both competitive yields and superior overall service quality, creating partnerships that support broader financial goals beyond simple savings accumulation.

Future Trends in High-Yield Savings Innovation

The evolution of money management automation continues to drive innovation within the high-yield savings sector, with emerging trends suggesting increasingly sophisticated and personalized banking experiences. Artificial intelligence integration promises to revolutionize how banks interact with customers, offering predictive savings recommendations, automated financial health assessments, and personalized yield optimization strategies. These advancements will likely make high-yield savings accounts even more effective wealth-building tools by eliminating behavioral barriers and maximizing returns based on individual financial patterns and goals. The continued improvement of user interfaces and experience design will make sophisticated financial management accessible to broader audiences, democratizing wealth-building capabilities.

Blockchain and distributed ledger technology present potential future applications for high-yield savings accounts, particularly around transparency, security, and transaction efficiency. While mainstream adoption remains uncertain, the underlying technology could enhance how banks verify transactions, prevent fraud, and document account activity. The integration of decentralized finance principles might create hybrid models that offer traditional banking security with innovative yield generation mechanisms. These developments would represent the next evolution in digital banking, building upon the foundation established by current online banking platforms. The pace of technological change suggests that high-yield savings accounts will continue evolving rapidly, offering increasingly attractive combinations of yield, security, and convenience.

Regulatory developments will shape the future landscape of high-yield savings accounts, with potential changes to deposit insurance limits, banking compliance requirements, and consumer protection standards. Understanding these regulatory trends helps investors make informed decisions about account selection and fund allocation strategies. The ongoing digital transformation of banking will likely prompt regulatory updates addressing emerging risks and opportunities within online banking environments. These changes will influence how banks structure their offerings, the yields they can provide, and the features they can offer customers. Staying informed about regulatory developments ensures investors can adapt their strategies to maximize benefits while maintaining compliance and security within evolving banking landscapes.